The financial controller’s relationship with AP is different from the AP manager’s.

The AP manager feels the daily friction, the inbox chasing, the re-keying, and the supplier queries. The financial controller owns the risk. When the auditor asks how a specific invoice was approved, it’s the financial controller who must answer. When a payment goes to a fraudulent account, it’s the financial controller who takes the call. When the month-end close runs three days late because of a backlog of unapproved invoices and a reconciliation full of coding errors, it’s the financial controller’s close.

That distinction matters when thinking about AP automation. This isn’t a tool that makes the AP team’s day easier, though it does that too. It’s a tool that closes the gaps that create personal professional risk for the controller: the audit trail gap, the fraud control gap, the month-end ownership gap, and the eInvoicing compliance gap.

Each of these four pressures is manageable in isolation. Combined, they make a clear case, not just for AP automation as an efficiency project, but as a risk management priority.

Pressure — What it costs when it materialises

Audit trail gap — Hours or days of email archaeology to reconstruct the decision history on a single invoice. Exposure in every audit.

Fraud exposure — A single BEC (business email compromise) payment to a fraudulent account. The financial controller is the person who has to explain the loss to the CFO and the board.

Month-end ownership — A close that takes five days and shouldn’t. Two of those days are rework, and chasing that AP automation would have been eliminated before the month ended.

eInvoicing compliance — Being asked ‘Are we ready?’ by the CFO with no credible answer, or by a government customer who requires Peppol eInvoices.

The Audit Trail Gap

An auditor asks you to produce the decision history on invoice #4721. Date received, who coded it, how it was approved, under which delegation authority, by whom, at what time, and what the final posting was.

In a manual AP environment, that reconstruction takes hours. The invoice arrived by email. Find the email. It was forwarded for approval, find that chain. The approval came back, find the reply. The coding was done by someone in the AP team; check their notes, if any exist. The ERP shows the posting, but if the GL code was wrong and corrected, the history of the correction may live in a separate journal, approved via a different email thread.

This is the audit trail that email-based AP produces: fragments distributed across inboxes, with no guarantee they’re complete, no timestamp authority that would satisfy a rigorous audit, and no structured link between the approval decision and the invoice it relates to.

A proper AP audit trail records who approved each invoice, exactly when, under which delegation rule, the GL code applied and why, any exceptions raised and how they were resolved, and the final ERP posting, all of it linked to the source invoice and retrievable in a single query.

For the financial controller, this is not an abstract compliance benefit. It’s the difference between a two-minute audit response and a two-day one. It’s the difference between an audit that confirms controls are working and one that surfaces gaps you didn’t know existed. And increasingly, with ATO compliance activity targeting GST treatment and cost allocation, the quality of the AP audit trail is a direct indicator of the financial control environment.

Fraud Exposure Through Weak AP Controls

Business Email Compromise is consistently one of the most financially damaging fraud types targeting Australian businesses. The ACCC’s (Australian Competition and Consumer Commission) Scamwatch data identifies it as responsible for hundreds of millions of dollars in annual losses, with mid-market businesses disproportionately affected.

The mechanism is straightforward. A fraudster gains access to or spoofs a supplier’s email address. They send a plausible invoice or bank account update request. An employee, following the same informal email-based process they use for every approval, processes it. The money moves before anyone notices.

A composite example drawn from the ACCC reporting pattern: a business receives what appears to be a routine invoice from a regular supplier. It’s forwarded for approval via email. The approver replies ‘approved.’ AP processes it against a bank account that was updated in the supplier record three weeks earlier, by someone with access to that supplier’s email domain. The payment clears. The fraud isn’t discovered until the real supplier follows up on an unpaid invoice.

The financial controller is the person responsible for explaining this loss. Not the AP team member who processed the payment, they followed the same process they use for every other invoice. Not the approver who replied to the email, they received something that looked legitimate. The failure is structural, in the controls that weren’t present.

Structured AP workflows close this gap at the architecture level:

- Supplier bank details are locked. Changes require a verified update process, not an email reply.

- Invoices are matched against supplier master data. Anomalies, including bank account and Tax ID, must match or be reviewed and released by the AP team before proceeding.

- Approval workflow is system-governed. The approval decision is logged, timestamped, and linked to the invoice. There’s no informal email chain that a fraudster can join.

- Delegation of authority is enforced by the platform. An invoice above a defined threshold can’t be approved at a lower required seniority level, regardless of who forwards it or how it’s worded.

These aren’t controls that need to be designed from scratch. They’re the default architecture of a modern AP platform. The financial controller who implements AP automation isn’t adding a fraud control layer on top of an existing process, they’re replacing a process that has no control layer with one that does.

Month-End: The Cost the Financial Controller Owns

Month-end close exposes every AP inefficiency that accumulated during the preceding 25 days. The financial controller doesn’t just observe this — they own it.

Three mechanisms drive the month-end pressure in a manual AP environment. The approval backlog: invoices that didn’t clear the email chain before cut-off, requiring finance to chase approvals and run the close simultaneously. The coding rework: GL errors that were invisible during processing and surfaced only at reconciliation, requiring journals, re-approval, and re-reconciliation. And the accruals gap: no live view of outstanding invoices, so accruals are estimated from memory rather than built from data, and sometimes are materially wrong.

AP automation changes the month-end dynamic before close begins, not during it.

- Approvals completed during the month. Workflow automation routes each invoice automatically, enforces cut-off rules, and escalates to a delegate when the primary approver is unavailable. The backlog doesn’t exist at month-end because it was prevented during the month.

- Coding errors caught at entry. Business rules validate GL code, cost centre, entity allocation, and tax treatment at the point of processing, not at reconciliation. Errors that used to require month-end journal entries are prevented before posting.

- Accruals built from data. An outstanding invoice dashboard shows every invoice in the workflow, received but not yet approved, approved but not yet posted, in real time. The financial controller arrives at close with a complete picture of what’s outstanding, not an estimate.

The result isn’t a faster scramble. It’s a different kind of close, one where the financial controller is validating what the system already reflects, rather than assembling what it doesn’t.

The eInvoicing Compliance Question

Australia’s eInvoicing mandate, built on the Peppol network, is expanding. Commonwealth government agencies are already required to receive Peppol eInvoices. Further compliance stages are on a known trajectory toward 2026 and beyond. The financial controller at any ANZ business with government customers or suppliers will be asked, by the CFO, by a procurement team, by the customer, whether the business is ready.

‘Ready’ has a specific meaning in this context. It doesn’t mean ‘we’ve heard of Peppol.’ It means the AP platform receives Peppol-formatted eInvoices natively and routes them through the same workflow as PDF invoices, without a manual conversion step, a separate process, or an OCR layer that reintroduces the data quality problems eInvoicing was designed to eliminate.

The platform question to ask: does your AP platform receive Peppol eInvoices natively, or does it convert them to PDF and run them through an OCR extraction process? These are not equivalent. A Peppol eInvoice that goes through OCR extraction has lost the structured data quality that makes eInvoicing valuable. The compliance box may be ticked, the operational benefit isn’t.

The financial controller who builds Peppol-native AP capability now isn’t scrambling to meet a deadline; they’re ahead of it. As Peppol adoption grows in the supplier base, eInvoices begin appearing in the workflow automatically. The processing cost for those invoices drops materially: no extraction step, no validation of extracted data, straight-through processing for compliant invoices.

For multi-entity ANZ groups, the compound effect is significant. Each entity’s eInvoicing readiness is managed within the same platform. Peppol eInvoices from common supplier’s flow into multiple entity workflows without separate setup. The financial controller who builds this now has a compliance foundation that scales with the business rather than one that needs to be rebuilt as entity count or supplier Peppol adoption grows.

Building the Case for Your CFO

The financial controller is almost always the AP automation champion. They experience the four pressures directly, understand the structural nature of the problem, and can translate the operational detail into a business case. The CFO’s question is simpler: what does this cost, how long does it take, and what risk does it close?

The financial controller who brings all three gets the conversation.

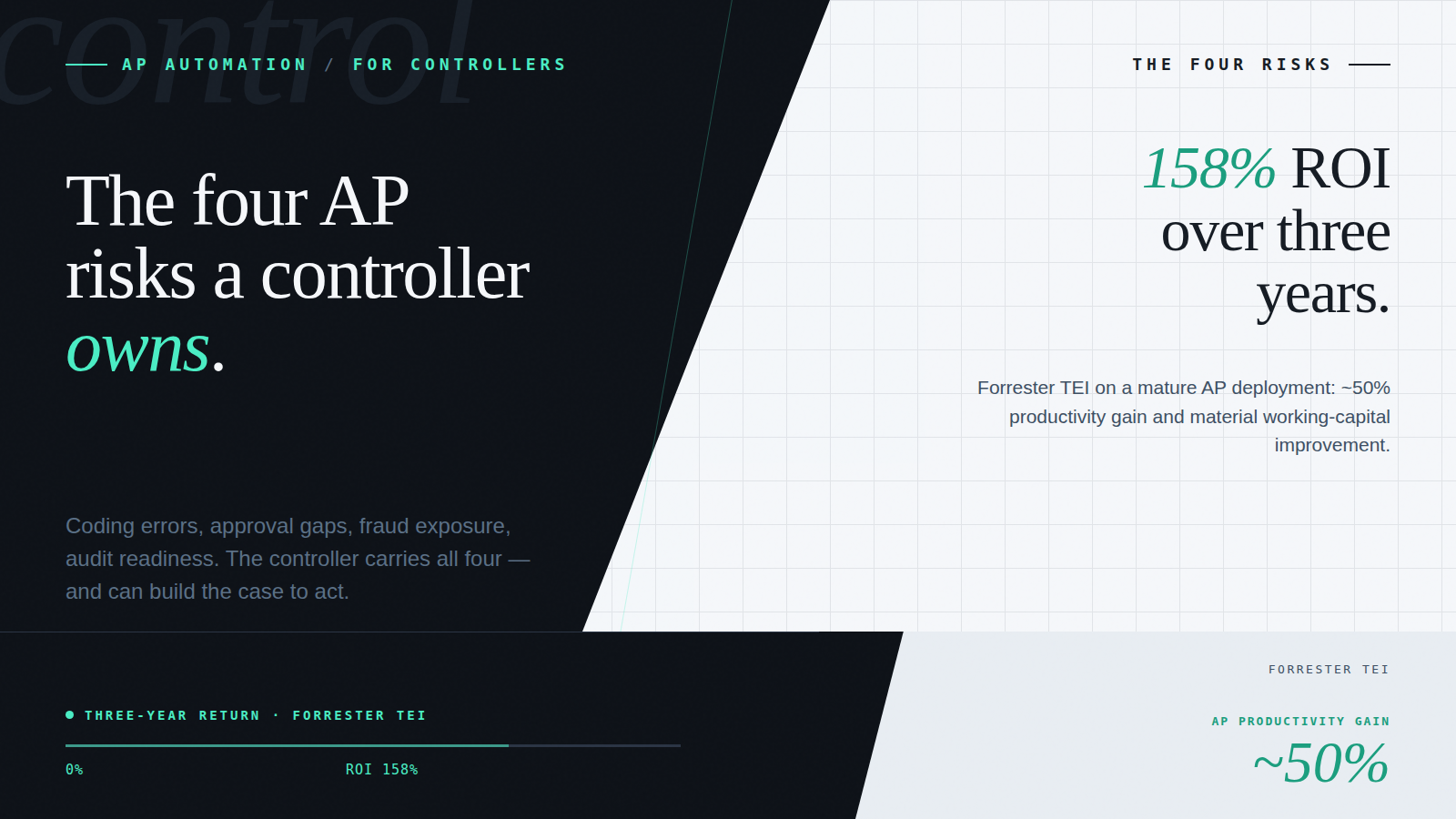

The number Processing cost eliminated + headcount redeployment + fraud prevention. The ATO benchmarks manual PDF processing at ~$27/invoice. At 400 invoices/month, that’s $129,600/year at risk. — The timeline Four to eight weeks to live processing for ANZ mid-market ERP. Not a 12-month enterprise IT project, a finance-led deployment with pre-configured rules. — The risk frame Audit exposure, fraud controls absent, eInvoicing compliance deadline. The CFO who hears the risk frame alongside the ROI frame doesn’t ask ‘why now?’ they ask ‘why haven’t we done this?’

One note on the timeline: AP automation for ANZ mid-market businesses is not a 12-month IT project. It’s a four-to-eight-week finance-led deployment. Implementation doesn’t require IT resource to build business rules from scratch, a modern ANZ AP platform comes pre-configured with rules based on AP best practice, adjusted for your specific structure. That distinction matters for the CFO who associates the ‘automation project’ with enterprise implementation timelines. The work is in the ERP integration, which, with willing parties on both sides, is about ensuring the supplier, general ledger, purchase order and processed invoices can be imported by the system.

The Business Case for AP Automation Blog covers the ROI calculation in detail, including how to model processing cost reductions, headcount redeployment, and fraud-prevention value. This piece is the controller’s half of the toolkit; that one is the CFO’s.

Ready to See It in Practice?

Acume is built for the ANZ mid-market: pre-configured AP business rules based on best practice, native Xero and MYOB integration, Peppol-native eInvoicing, and an implementation model that deploys in weeks rather than quarters.

If you’re the financial controller who’s been meaning to address the four pressures described in this piece, the most useful next step is a conversation about your specific AP environment, invoice volume, ERP configuration, approval structure, and eInvoicing readiness. We’ll map what the workflow looks like for your business specifically.

Frequently Asked Questions

How do I justify AP automation to my CFO?

Lead with three things: a number (current processing cost vs automated cost, at your invoice volume, the ATO benchmark is ~$27 for manual PDF processing), a timeline (four to eight weeks to live, not a 12-month project), and a risk frame (audit trail gaps, fraud exposure, eInvoicing compliance deadline). The Business Case for AP Automation guide in this series provides the full ROI model.

How long does implementation actually take?

For ANZ mid-market businesses on Xero or MYOB, four to eight weeks from contract to live processing is typical. The key variable is approval hierarchy complexity; businesses with straightforward single-entity structures deploy faster, and multi-entity groups with complex delegation rules take longer. A platform with pre-configured AP business rules deploys faster than one that requires custom rules built from scratch.

What does implementation require from IT?

Very little, for most ANZ mid-market implementations. Modern integrations to ERP should connect via API, we can also work with flat files if that is what your ERP or accounting platform can output. The business rules, approval workflows, and ERP export configuration are set up by the implementation team using pre-configured templates adjusted for your specific structure. The financial controller and AP lead are the primary stakeholders; IT is typically involved only if there’s a legacy ERP or non-standard integration requirement.

Will it work with our Xero or MYOB setup?

Yes. A purpose-built ANZ AP platform integrates natively with Xero and MYOB, syncing suppliers, GL codes, tax logic, and cost centre structure directly from your accounting system. Approved invoices export to Xero or MYOB via API in real time. For businesses with a legacy ERP behind the primary accounting platform, middleware integration is available, the Bridging the Legacy Divide Blog covers the integration architecture in detail.

What about our current volume – is it enough to justify this?

The break-even point for AP automation varies by invoice volume and current processing cost, but most ANZ mid-market businesses processing 200 or more invoices per month find that the processing cost savings alone cover the platform subscription within six to twelve months. The audit trail, fraud control, and month-end benefits are additional, and they’re not volume-dependent. A fraud incident or an audit gap costs the same whether you process 200 invoices a month or 2,000.

A demo on your actual workflow.

A live walkthrough using real data – the capture, the coding, the approval routing – and how it sits inside the AP workflow you already run. No slideware.