In 2025, businesses in Australia and New Zealand are navigating an uncomfortable reality: fraud risk has shifted from occasional anomaly to operational inevitability, especially in Accounts Payable.

Behind every delayed payment, mismatched invoice, or hastily approved supplier sits a potential breach point. And the cost of getting it wrong isn’t just financial — it’s trust, compliance, and reputational standing.

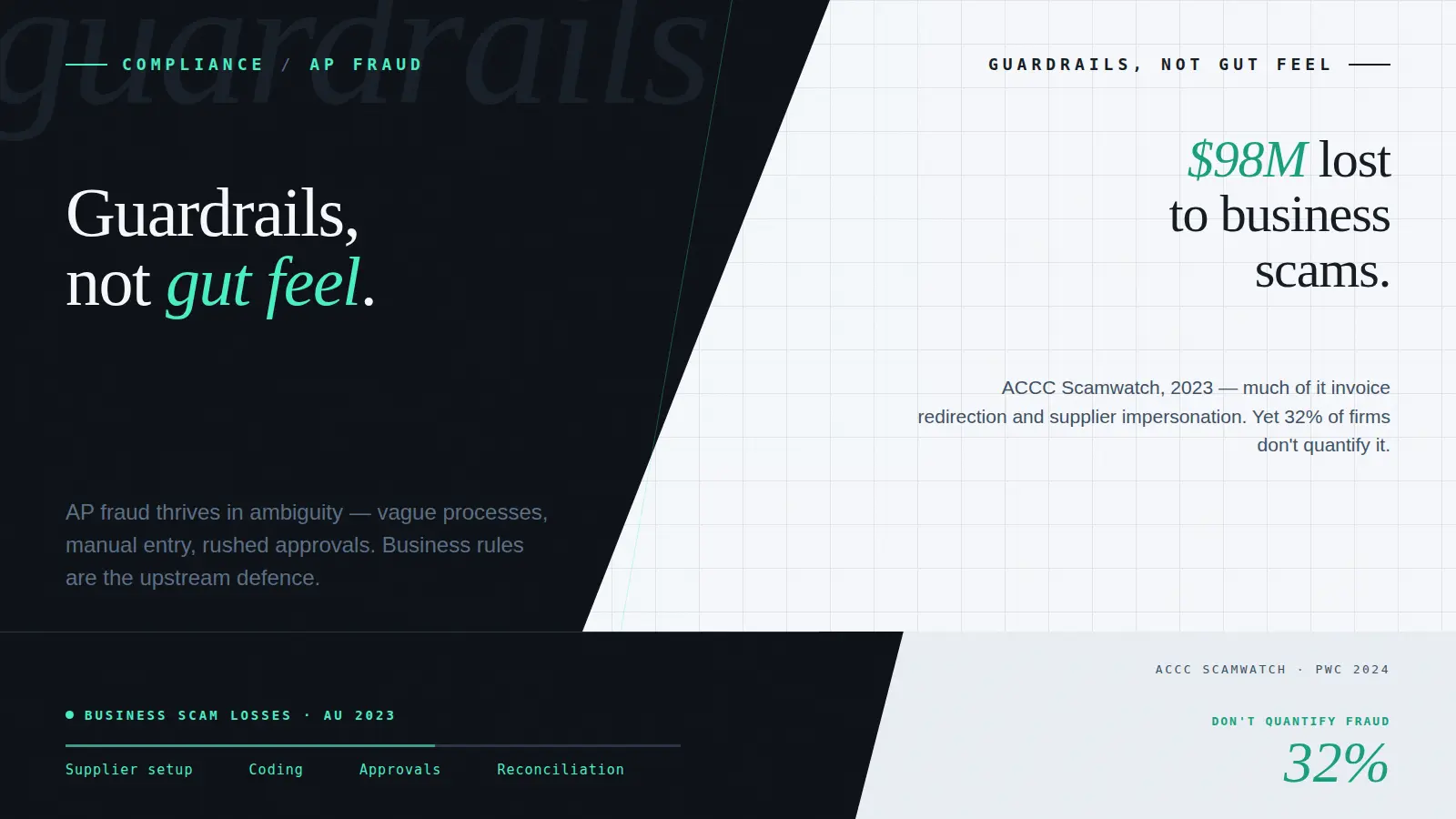

In both countries, while phishing scams and social engineering dominate headlines, the slower-burning threat of Accounts Payable and procurement fraud is quietly eroding business margins across both countries.

- Australia: The ACCC’s Scamwatch reported over $98 million in business losses to scams in 2023 alone, with a significant share tied to invoice redirection fraud and supplier impersonation.

- Globally, procurement fraud (a close cousin of AP fraud) ranks among the top three most disruptive economic crimes, according to PwC’s 2024 Global Economic Crime Survey. Yet, 32% of businesses still don’t even quantify the impact of this fraud category.

What Makes AP So Vulnerable?

Unlike overt cyberattacks, AP fraud thrives in ambiguity: vague processes, manual data entry, or rushed approvals. Fraudsters — external or internal — exploit weak or absent controls in areas like:

- Supplier creation and validation

- Manual invoice coding

- Weak approval workflows

- Lack of real-time reconciliation

Even trusted suppliers can become risk vectors if bank details change or documents are intercepted.

The Role of Business Rules as Guardrails

The most effective defence isn’t downstream detection, it’s upstream prevention.

Business rules are the digital equivalent of zero-trust architecture for finance teams: they validate assumptions, block risky transactions, and reduce human error. When embedded into AP systems, they become invisible enforcers of best practice.

Some non-negotiables Acume implements as standard:

- The supplier must already exist in the master file before an invoice is accepted

- GST/IRD numbers and bank accounts must match between the invoice and supplier record

- Invoices can’t be processed unless coded and approved via structured workflows

- Three-way matching (PO, invoice, receipt) is enforced where applicable

These aren’t just features, they’re fraud guardrails, built into the DNA of the platform.

Why This Matters Now More Than Ever

Deloitte’s 2024 Asia-Pacific financial crime outlook emphasised that regulators are increasingly targeting AP and procurement processes in fraud investigations. In both countries, directors are being asked to certify that adequate financial controls are in place, and AP is no longer exempt from scrutiny.

The old mindset of “we trust our people” doesn’t scale. As invoice volumes rise and payment fraud becomes more sophisticated, rigid, policy-enforced workflows are no longer optional; they’re the baseline.

What Can Finance Teams Do?

Whether you use an automation platform or still rely on spreadsheets, here are steps you can take today:

- Audit your supplier master file: How many are unverified or duplicated?

- Validate bank accounts and GST/IRD numbers against invoices

- Enforce mandatory approvals with named, role-based users

- Automate basic matching rules (invoice-to-PO, invoice-to-receipt)

- Review export and payment logs weekly for exceptions

Final Thought: Guardrails Are an Investment in Integrity

Fraud doesn’t always look like fraud. Sometimes it’s just a second invoice with a slightly different bank account. Or an urgent approval email that bypasses usual checks.

But these moments, if unchecked, are exactly where risk takes root.

By investing in enforceable business rules, you don’t just protect your payables — you protect your business, your people, and your reputation.

Where to Go Next

- AI in accounts payable: why guardrails matter more than hype – rules, audit trails and where AI should not decide.

- Supplier master data and invoice fraud prevention – your first line of defence against payment redirection.

- The hidden cost of email invoice approvals – what inbox approvals really cost.

- Accounts payable automation with Acume – the AP solution page.

A demo on your actual workflow.

A live walkthrough using real data – the capture, the coding, the approval routing – and how it sits inside the AP workflow you already run. No slideware.